The Great Talent Misallocation

Why top talent keeps flowing to finance, and what the evidence says about whether that's a problem.

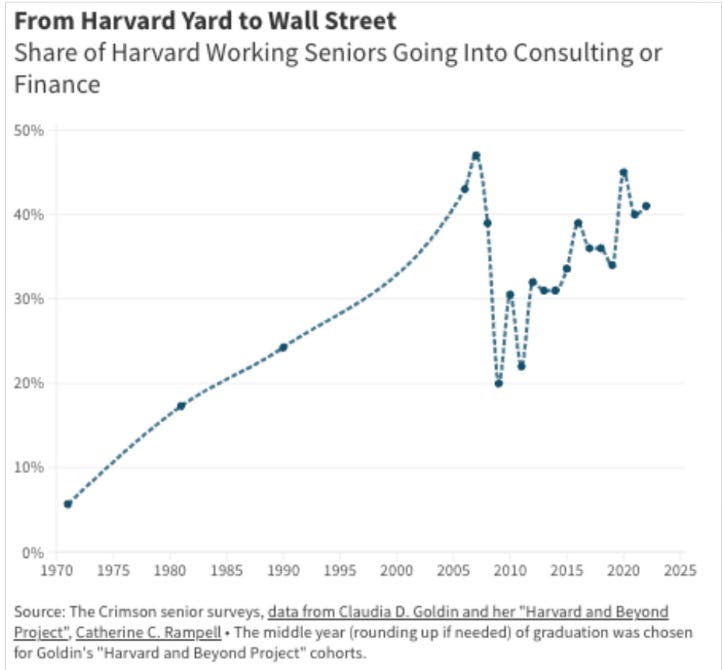

This chart lives rent-free in my head. It's the phenomenon Simon Van Teutem and Rutger Bregman have talked about: in the Western world, more and more talent has been flowing to a narrow set of jobs. Finance, consulting, corporate law.

Wages are set by supply and demand, so on paper this should be roughly efficient. But anecdotally, it feels dislocated. These sectors pay extremely well, and it's not always clear what they're producing that justifies it. Have wages here outrun the value being created? (Econ 101 primer on the labour market here)

Note: I’ll use finance as the lens throughout because the data is cleanest there. The same logic plausibly extends to other high-scalability sectors, but with cruder evidence.

A simple model of talent and scalability

For most knowledge work sectors, the interaction between firms and workers can be thought about using the following simplified model1

A is the talent of the decision-maker. Anyone whose effort moves the needle on firm output: CEO, manager, star trader, analyst, deal-maker, etc.

s is the common state of technology in the economy

f(H) is the production function: how output rises with headcount H.

W is the wage rate set by labour market demand and supply

This shows that profit is a function of the general ability and talent level of the firm, the common state of technology in the economy, and returns to employing labour in an industry, minus the wage bill.

Returns to labour have marginal diminishing returns as every additional worker is less valuable to the firm than the previous. We model this with:

Higher α means returns diminish more slowly. α is the scalability of labour in a sector.

We assume f(H) is similar for firms across the industry, and that s is common economy-wide. Both are reasonable as business models within an industry tend to converge, and technology diffuses as best practices get adopted. Wages are set by demand and supply, so an individual firm is a price taker. Hence, the key variable that a firm optimises to maximise profit is H.

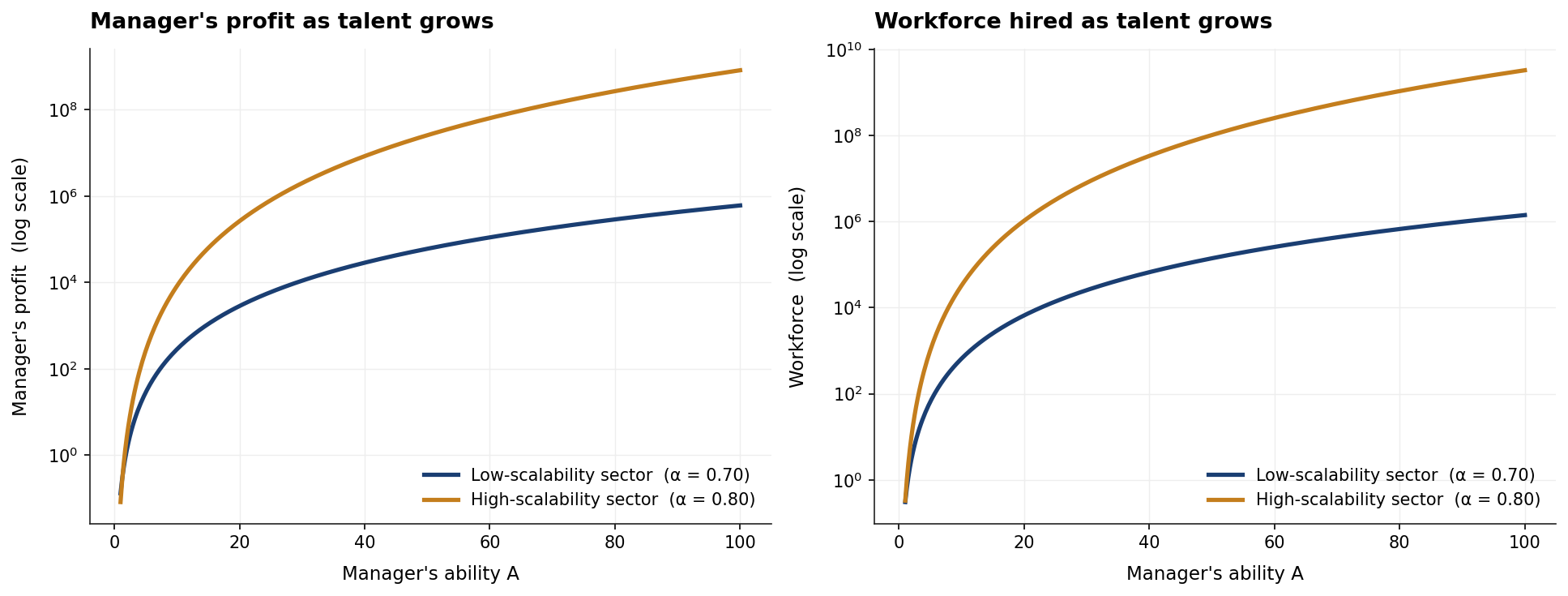

Solving for the profit-maximising H and plugging back in, both the firm’s headcount and its profit are proportional to talent, levered by the sector’s scalability:

That single exponent does almost all the work in this model. If you want to feel its leverage, there's a dashboard where you can vary α and A and watch the curves move; the full derivation lives there too.

As seen in Fig 2, for each level of ability, profit and headcount are exponentially higher in the more scalable sector, and the gap widens with ability.

Take a restaurant and a financial firm. The restaurant hits its ceiling fast. Once the tables are full and the kitchen is at capacity, hiring more cooks doesn’t help. A financial firm doesn’t have that problem. Hiring another analyst means more clients to manage and more capital to deploy, and there’s no obvious upper limit to how far that scales. Similarly, give either firm a small advantage in talent, and the difference between sectors becomes obvious. A 1% edge in ability earns the restaurant manager a few extra covers a night. The same 1% edge in the financial firm can earn the manager millions in additional profit. It’s the same talent in both cases, but the exponent in each sector amplifies it very differently.

What the French data shows

This is still a theoretical framework. What does this look like in the real world?

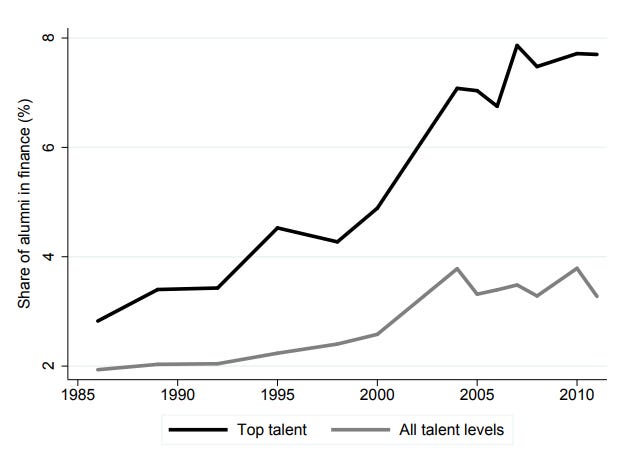

In 2019, Célérier and Vallée wrote a paper that maps closely onto this question. France has a system of elite universities called the Grandes Écoles. At 18, students take a national multi-disciplinary entry exam whose rank determines which school they get into. The authors used over 300,000 survey responses from engineering graduates between 1983 and 2011, with exam performance as a clean proxy for talent. The setup lets them isolate which sectors reward talent more steeply, holding talent itself constant.

Plotting wage premiums against school selectivity, you see finance has a far steeper slope than every other sector. A graduate from a school 10 percentage points more selective earns ~5% more in finance against only ~2% more in the rest of the economy. The same fractional improvement in talent is rewarded close to three times over in finance. This is exactly what we'd expect if finance has a higher α.

The model predicts higher profit in high α sectors; the paper measures higher wages. These are linked. In a competitive market, firms bid for talent, and the ones that capture the most profit per worker bid hardest, so the convexity in profit gets passed through to wages. Modern comp contracts (equity, options, carry) make the link explicit.

As a result, more graduates flock towards finance over time, but this is especially true among the most talented graduates (those from the most selective schools). Their share going into finance rose from around 3% in 1986 to over 8% by 2011. Top talent has been absorbed into finance at a disproportionate rate, and the gap has widened over time.

France is one example, but similar finance wage premiums are observable in many developed countries.2

When does this become a misallocation?

The finding itself that higher α sectors attract more talent doesn’t point to a misallocation. It’s simply a commentary on how hiring dynamics work across sectors. Pharma R&D is high α and we want talent flowing there. The misallocation shows up when α isn't tracking social value, and finance is the cleanest case where this seems to happen.

It is well documented that financial development is important for economic growth: it facilitates access to credit, supports entrepreneurship, and reduces investment friction. It clearly has a role in society. But past a point, more finance is plausibly crowding out talent and capital that the rest of the economy could use.

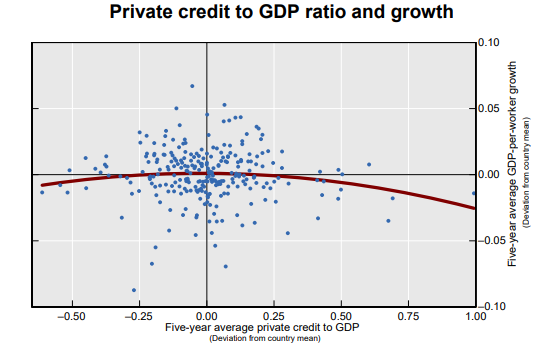

This is what Cecchetti and Kharroubi observe. Testing several measures of financial-sector size across many countries, they find an inverted-U relationship with economic growth: more finance helps up to a point, then is associated with slower growth.

One measure is private credit as a share of GDP.3 Within a country, more private credit is initially associated with above-trend GDP growth, but past a turning point, it's associated with slower growth. Across countries, that turning point sits at around 90% to 100% of GDP.

Today, private-sector credit sits at around 140% of GDP in the US and 133% in the UK. Both are well past the range where additional financial deepening is associated with growth.

Neither paper proves the misallocation story by itself. Célérier and Vallée show top talent flows steeply to finance. Cecchetti and Kharroubi show that past a threshold, more finance is associated with slower growth. We make the connecting assumption that the marginal workers in finance are contributing towards the unproductive bit.

Why did finance pull away?

Three forces have raised the returns to talent in finance over the last few decades. Technology is the first: computing power and electronic markets turned each skilled person into a much larger productive unit, which raises α directly. Compensation contracts are the second: equity, options, and carry tie individual pay to firm-level outcomes, so when α rises, top earnings follow. Both reflect real productivity gains, and neither is the problem.

The third force, and the one this section spends its time on, is policy. The two landmark moments below were defensible at the time as moves toward more competitive markets. What they also did was raise α, with talent-allocation consequences no one had on their mind when the policies were designed.

Big Bang, 1986. Until the mid-1980s, the London Stock Exchange ran under restrictive rules. Trading commissions were fixed at high levels. Jobbers (the market-makers who held inventory) and brokers (the dealers who served clients) had to be separate firms. Foreign banks couldn’t own UK firms. The Big Bang in October 1986 swept all of that out in a single weekend. Fixed commissions and the jobber-broker separation went, and foreign ownership opened up. Smaller UK firms got bought by larger international banks, and a much bigger, more capital-intensive industry took shape almost overnight. Big balance sheets, more deal-making, more proprietary trading.

Glass-Steagall repeal, 1999. The Glass-Steagall Act of 1933 had kept commercial banking (taking deposits, making loans) separate from investment banking (underwriting securities and trading on a firm’s own account). The Gramm-Leach-Bliley Act of 1999 repealed that separation. Banks could now be one-stop financial supermarkets. The investment-banking side scaled onto the deposit-funded balance sheet, and the talent intensity at the top of the industry rose sharply.

After 2008, parts of this were reversed.4 The UK introduced ring-fencing rules that re-separated retail banking from investment banking. The US passed the Volcker Rule to restrict proprietary trading at deposit-taking banks. Basel III pushed up capital requirements globally. But the net effect was mostly to push the same activities outside the regulated banking sector rather than shrink them. Hedge funds, private credit funds, quant trading firms, and more recently prediction-market platforms absorbed what banks had to step back from. The same high α work is still happening; the regulated banking sector just has less of it.

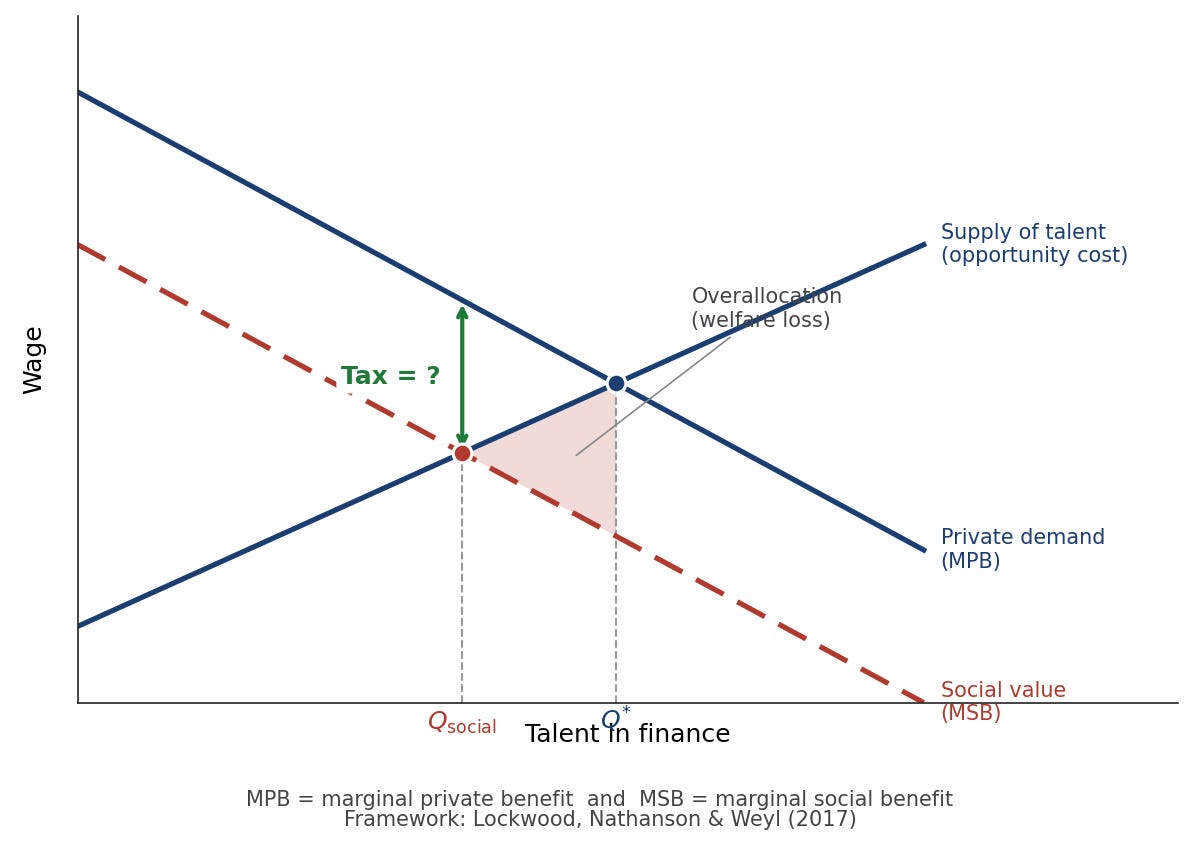

What we can and can't fix

If this really is a misallocation, the textbook answer is to make the misallocated activity more expensive on the margin. That’s a Pigouvian tax: charge for the externality, push private cost in line with social cost, let the market re-sort.

The problem is measuring welfare loss. To set the right tax, you have to know the social cost of the marginal finance worker, which is something no one has a great handle on. Cecchetti and Kharroubi give you a credit-to-GDP threshold, but that's a long way from "tax each extra hour of trader time at $X." Set the rate too low, and you do nothing. Set it too high, and you push activity offshore, into the shadow sector, or onto less-skilled people who do the same job worse.

Some workarounds don’t require knowing the exact tax. Singapore pays its ministers and senior civil servants on a benchmark tied to top private-sector earners, partly to keep talented people from being pulled into finance and law by default.

Outside of market mechanisms, some efforts try to nudge talent flow directly. Rutger Bregman’s School for Moral Ambition recruits high-performers out of corporate jobs and channels them toward neglected problems. Ambitious Impact does something similar for the social-impact pipeline.

Talented people are sorting into high α sectors because that’s where their work gets levered most. Where α tracks real social value, that’s the invisible hand at work. In finance, past a certain size, the evidence makes it harder to claim.

That’s about all the evidence supports right now. No one has measured the externality cleanly enough to set a tax around it or build anything else to close the gap. Same picture probably extends to consulting, law, parts of big tech with messier data.

How to close any of these gaps is still an open question.

This model is adapted from Murphy, Shleifer & Vishny, 1991.

Philippon and Reshef, 2013 show finance wage premiums for other countries.

BIS definition: credit to the non-financial private sector from banks plus other lenders, as a share of nominal GDP.

Ring-fencing: UK rules requiring large banks to legally separate retail deposit-taking from investment banking. Volcker Rule: US restriction on proprietary trading at deposit-taking banks. Basel III: international capital and liquidity standards that raise the cost of holding risky balance sheet assets.

Very cool read, do you have any other interesting findings about aligning incentives - is it mostly a payoff problem or also prestige + generally lacking info at a young age about high-impact, low-status roles? What's the biggest leverage?

Nice read , I think and belive your generation @ Parth have to solve this problem as financialisation only helpvery few , it does not help the people or organsiations at a large or people as such , it serves only capitlist class, and they are biggest danger of capitalist model of economy